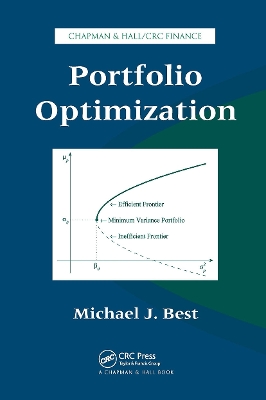

Portfolio Optimization

portes grátis

portes grátis

Portfolio Optimization

Best, Michael J.

Taylor & Francis Ltd

10/2024

238

Mole

9781032925967

15 a 20 dias

Descrição não disponível.

Optimization. The Efficient Frontier. The Capital Asset Pricing Model. Sharpe Ratios and Implied Risk-Free Returns. Quadratic Programming Geometry. A QP Solution Algorithm. Portfolio Optimization with Linear Inequality Constraints. Determination of the Entire Efficient Frontier. Sharpe Ratios under Constraints and Kinks. Appendix. References.

Este título pertence ao(s) assunto(s) indicados(s). Para ver outros títulos clique no assunto desejado.

Efficient Frontier;Minimum Variance Portfolio;francis;Risk Free Asset;group;Efficient Portfolios;efficient;Positive Semidefinite;frontier;Xmin Xmax Ymin Ymax;optimal;Portfolio Optimization;solution;Full Row Rank;minimum;Linear Equality Constraints;variance;Portfolio Optimization Problem;portfolios;Active Constraints;expected;Inequality Constraints;Risk Free Return;Sharpe Ratio;Optimal Solution;Linear Inequality Constraints;Nonnegativity Constraints;Maximum Sharpe Ratio;Active Inequality Constraints;Capital Market Line;Multiplier Vector;Market Portfolio;Parametric Interval;Inactive Constraints;Active Set

Optimization. The Efficient Frontier. The Capital Asset Pricing Model. Sharpe Ratios and Implied Risk-Free Returns. Quadratic Programming Geometry. A QP Solution Algorithm. Portfolio Optimization with Linear Inequality Constraints. Determination of the Entire Efficient Frontier. Sharpe Ratios under Constraints and Kinks. Appendix. References.

Este título pertence ao(s) assunto(s) indicados(s). Para ver outros títulos clique no assunto desejado.

Efficient Frontier;Minimum Variance Portfolio;francis;Risk Free Asset;group;Efficient Portfolios;efficient;Positive Semidefinite;frontier;Xmin Xmax Ymin Ymax;optimal;Portfolio Optimization;solution;Full Row Rank;minimum;Linear Equality Constraints;variance;Portfolio Optimization Problem;portfolios;Active Constraints;expected;Inequality Constraints;Risk Free Return;Sharpe Ratio;Optimal Solution;Linear Inequality Constraints;Nonnegativity Constraints;Maximum Sharpe Ratio;Active Inequality Constraints;Capital Market Line;Multiplier Vector;Market Portfolio;Parametric Interval;Inactive Constraints;Active Set